624 credit score area are middle-of-the-road, with scores below 631 significantly worse. One's creditworthiness is directly related to their FICO score, affecting their access to credit and interest rates. A credit score of 624 is not horrible, but it is below average and shows an opportunity for development.

Banks and other lending institutions use credit scores to assess the creditworthiness of potential borrowers. Credit scores over 670 indicate careful borrowing and timely payments and are preferred. Lower credit ratings, on the other hand, are associated with a greater propensity for late or missed payments. A credit score of 624 may make getting loans or credit cards more accessible, resulting in higher interest rates and fewer favorable terms.

Ranges of Credit Scores

Here are some typical credit score ranges to keep in mind:

Excellent (800 And Above)

If your credit score 624 or higher, you have outstanding credit. People in this bracket often have a spotless payment history, a low credit utilization ratio, and a lengthy credit history. They are candidates for the best possible loan, credit card conditions, and interest rates.

Very Good (740-799)

The range of credit scores from 750 to 850 is considered excellent. Individuals with credit scores in this range are considered safe bets by lenders. They can expect to qualify for various financing options at reasonable interest rates.

Good (670-739)

An excellent credit score falls between the 624 credit score car loan and 739. Persons with scores in this range have maintained their credit reasonably well, with only occasional slip-ups like late payments or higher-than-average utilization rates. They might be able to get loans and credit cards, but they might need better rates.

Fair/Average (580-669)

Fair or average credit starts with a score of 580 and goes up to 669. People in this bracket will likely have a larger-than-average credit card load or a history of late payments. Lenders may see them as having moderate credit risks, making it difficult to acquire credit or resulting in less favorable conditions and higher interest rates.

Poor (300-579)

If your credit score is below 580, it isn't good. People in this bracket often suffer severe financial difficulties, including frequent payment delays, defaults, or even bankruptcy. They might need help getting credit, and even if they do, they might be stuck with exorbitant interest rates and few choices.

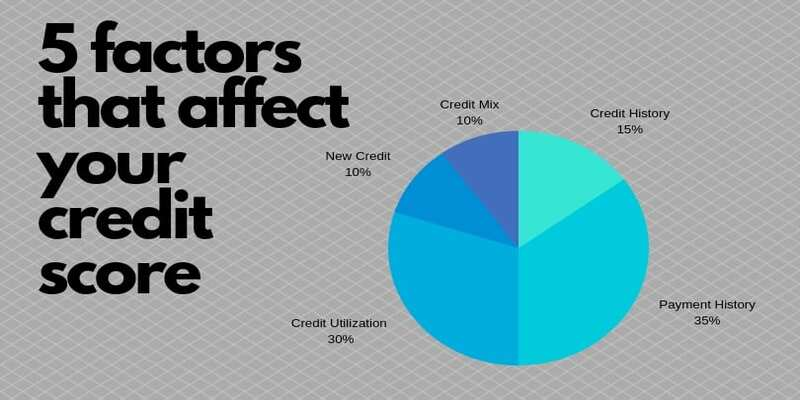

Factor Influence On Credit Score

Find out what influences your credit score below.

Payment History

The most crucial aspect of your credit score is your payment history. About 35% of your final grade depends on it. Creditors evaluate your payment history to determine if they should extend your credit. A credit score might take a severe hit in the event of late payments, defaults, collections, or bankruptcies. A good payment record is essential, so always pay your fees on time. This includes money owed on credit cards, loans, the mortgage, and everything else you owe. It's vital to prioritize paying payments on their due dates, as late payments can remain on your credit report for up to seven years. Talk to your creditors or lenders about setting up an alternate payment plan if you have trouble making payments.

Credit Utilization

The term "credit utilization" describes how much of your available credit you are using. It accounts for roughly 30% of your total credit score. Lenders favor borrowers whose credit utilization ratios are low. Credit utilization measures how much of your available credit you are using. If your credit limit is $10,000 and you're carrying a balance of $3,000, your utilization ratio is 30%. Maintaining a decent credit score requires keeping credit utilization below 30%. If your ratios are high, it could mean that you need help keeping up with your bills and are overly dependent on credit.

Conclusion

Credit scores in the 624 range are middle-of-the-road in quality but still below average. It's a good score but shows that your creditworthiness may use some work. Loans, credit cards, and reasonable interest rates can all be out of reach for someone with a credit score of 624. Remember that your credit score is not set in stone and can be raised gradually via sensible financial behavior. Paying on time, decreasing debt, and keeping a solid credit history are great ways to raise your credit score. Your creditworthiness might increase if you exhibit prudent credit behavior. You must also check your credit report frequently for any inaccuracies or irregularities that could drag your score down.